Selling your house this season? You’ve probably heard you should stage it before it hits the market. But what does that really mean – and is it worth the effort?

The short answer is “yes,” especially right now.

With more houses for sale this year, you’re likely wondering how to make the most money possible without your house sitting on the market. The answer is staging. It can help your house stand out, bring in stronger offers, and sell faster. As Nadia Evangelou, Principal Economist at the National Association of Realtors (NAR), puts it:

“Staging matters. Preparing the home to be ‘buyer-ready’ attracts more buyers, especially now that inventory has increased.”

Here's what staging actually involves and what it could do for your sale.

What Is Home Staging?

Home staging is the process of preparing your house, so it appeals to as many buyers as possible. That usually means decluttering, deep cleaning, rearranging furniture, and adding simple touches that help each room feel bright, open, and welcoming.

The goal is to help buyers fall in love with the space and picture themselves living there, which makes them more likely to make an offer.

Why Staging Is Worth the Effort

Staged houses tend to perform better on almost every metric that matters when you sell. According to Redfin, staged homes have been shown to sell up to 73% faster than unstaged homes. And they often close in under a month, compared to anywhere from two to three months for vacant ones.

There’s also a strong return on the money you spend.

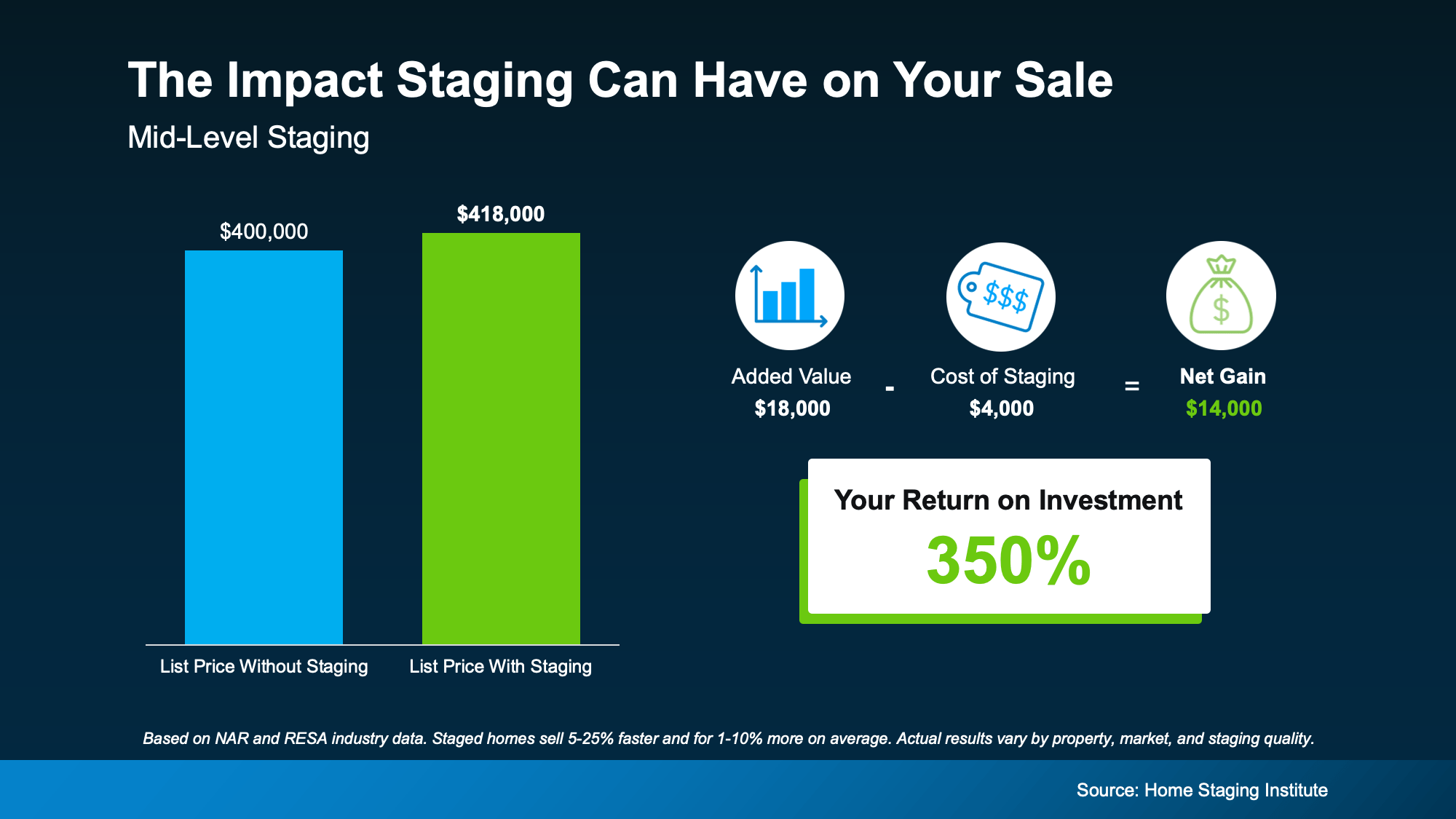

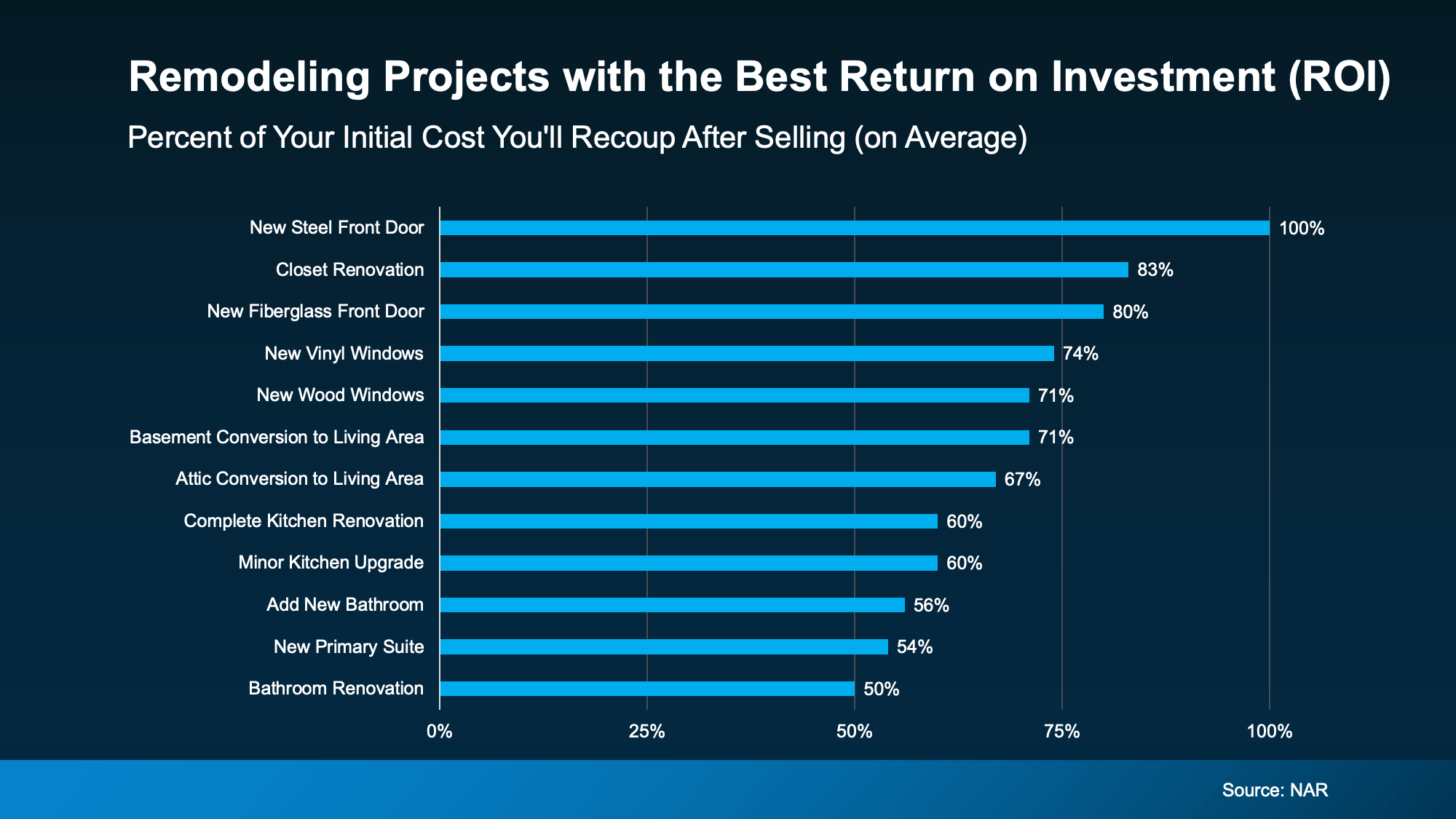

The Home Staging Institute says mid-level staging can deliver a 350% return on investment. On a $400k home, that turns the typical $4k cost into roughly $18k in added value when you sell (see graph below):

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

Your Staging Options

And just in case you’re seeing that $4k upfront investment above and thinking, “I’m not going to spend that,” here’s what you should know.

Staging doesn’t always have to mean hiring a full crew or filling your house with rented furniture. There are a few different paths you can take, depending on your budget and timeline. So, you could spend a lot less and still get a good return.

Here are a few options:

- Professional staging. A stager handles everything from layout to décor, often bringing in their own inventory. According to the Home Staging Institute, costs typically range from $500 to $5k or more, depending on the size of your house.

- Virtual staging. Digital furniture and styling are added to your listing photos, which can be a budget-friendly option for vacant houses.

- DIY staging. If your budget is tight and your home only needs minor updates, decluttering, deep cleaning, and arranging furniture for flow can still make a real difference.

Your agent can help you figure out which approach fits your house, your market, and your goals.

Agents see what buyers respond to in open houses and showings every week, so they can give you specific, personalized recommendations on what’s worth your time and money (and what isn’t).

That way you can get the most bang for your buck – no matter your budget.

Bottom Line

With more homes for sale right now, making a strong first impression matters. Staging can help your house sell faster and for more – and there's an option for almost every budget.

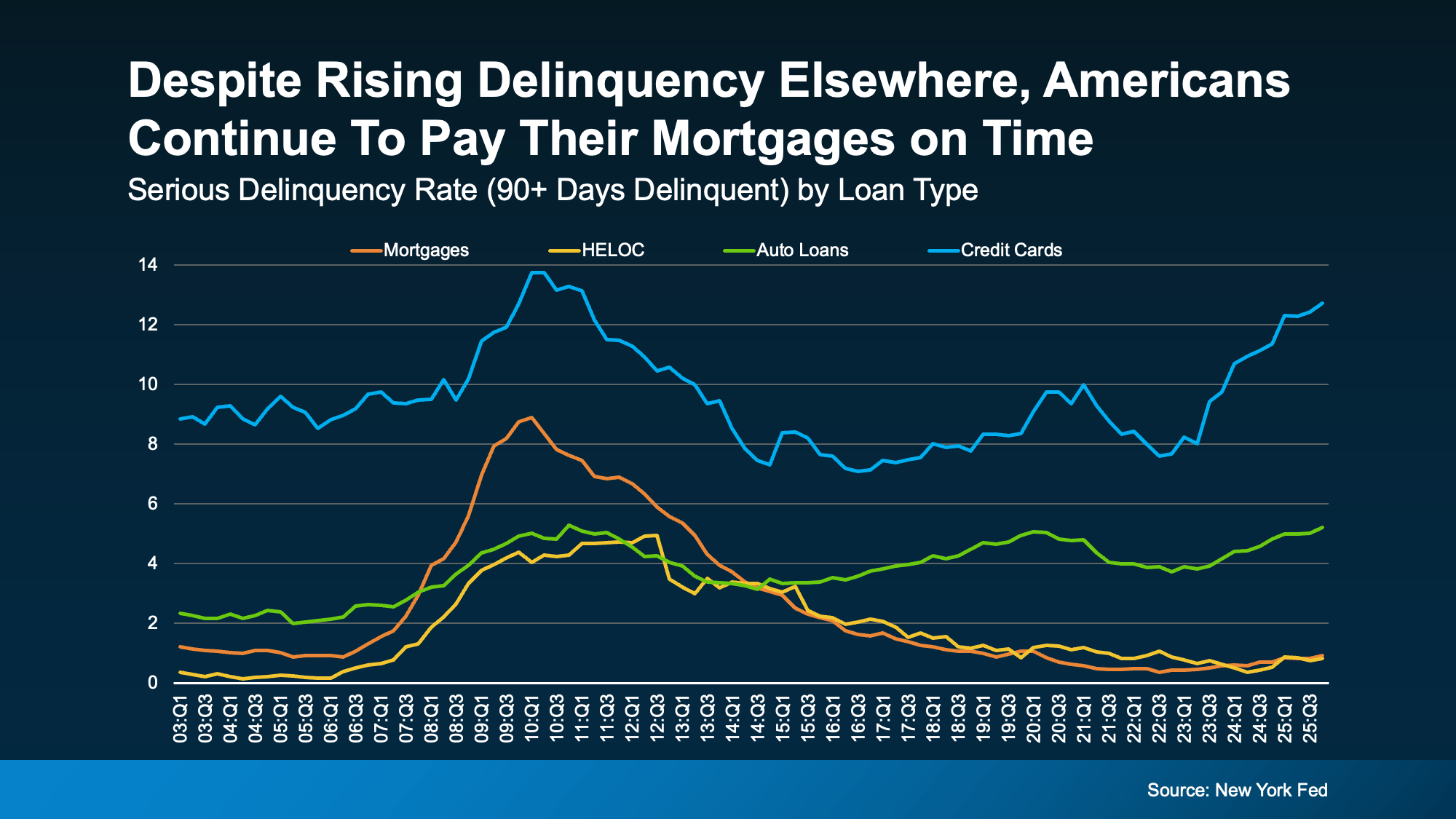

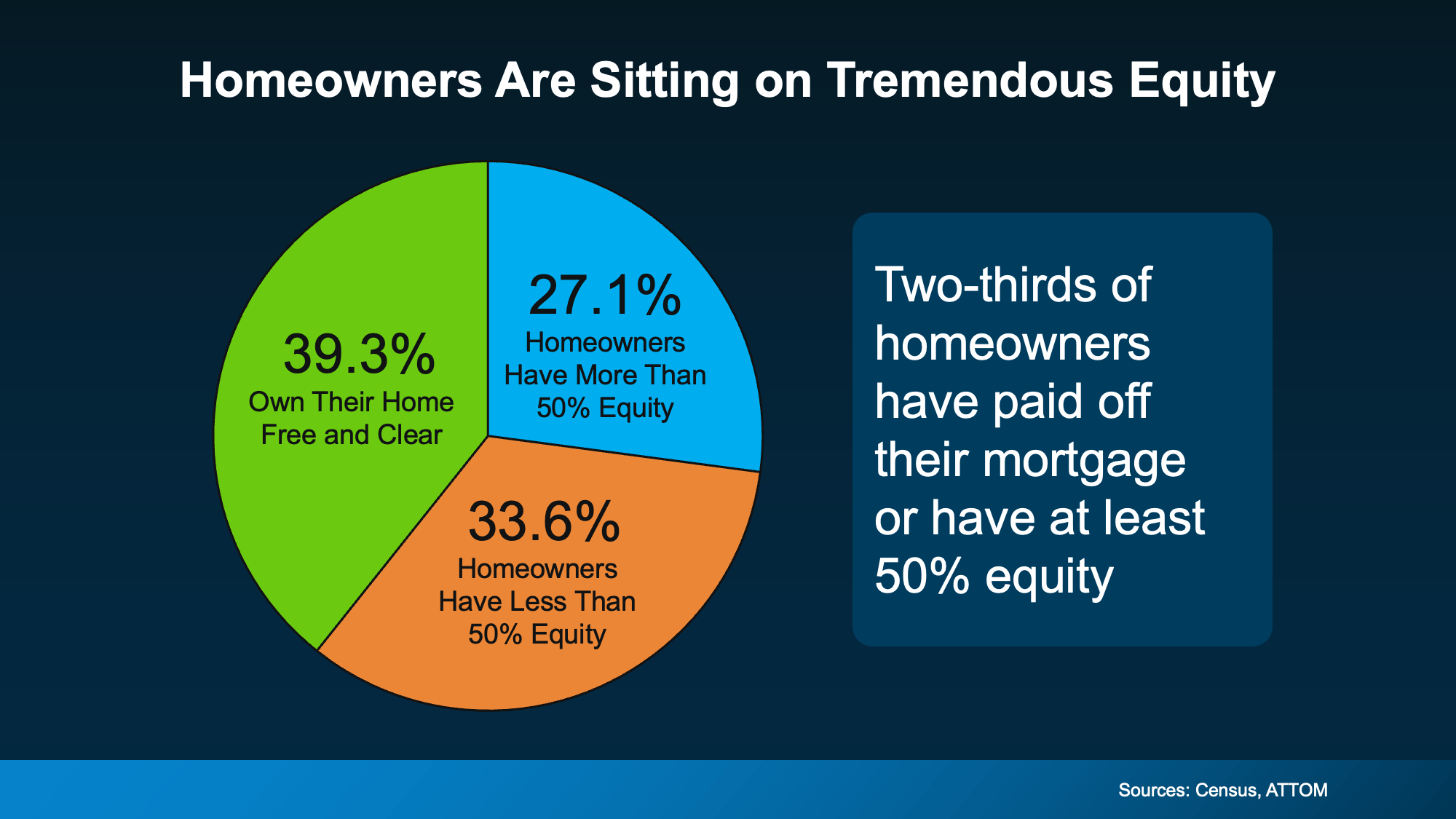

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

The Part Sellers Don’t See Coming

The Part Sellers Don’t See Coming

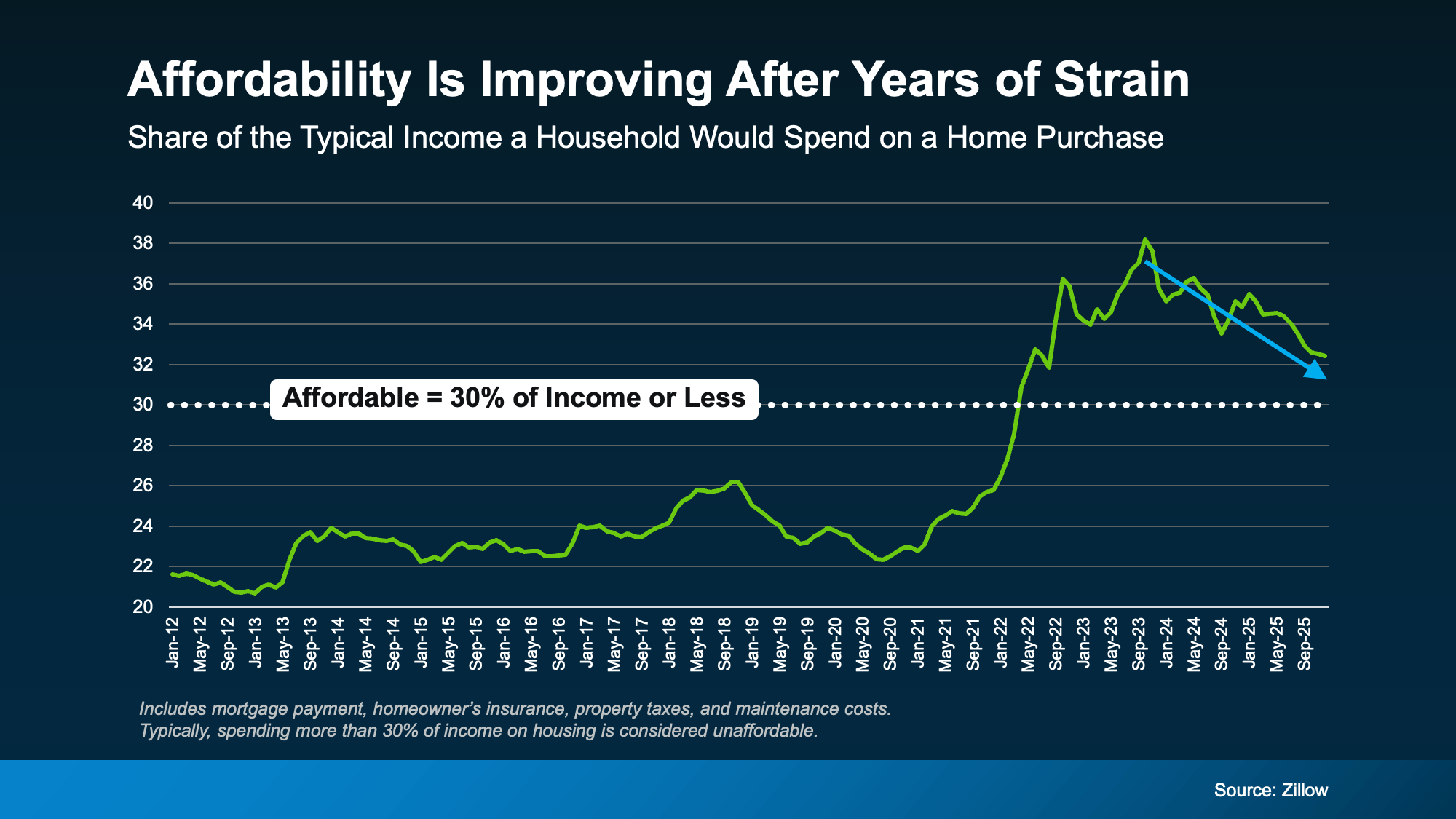

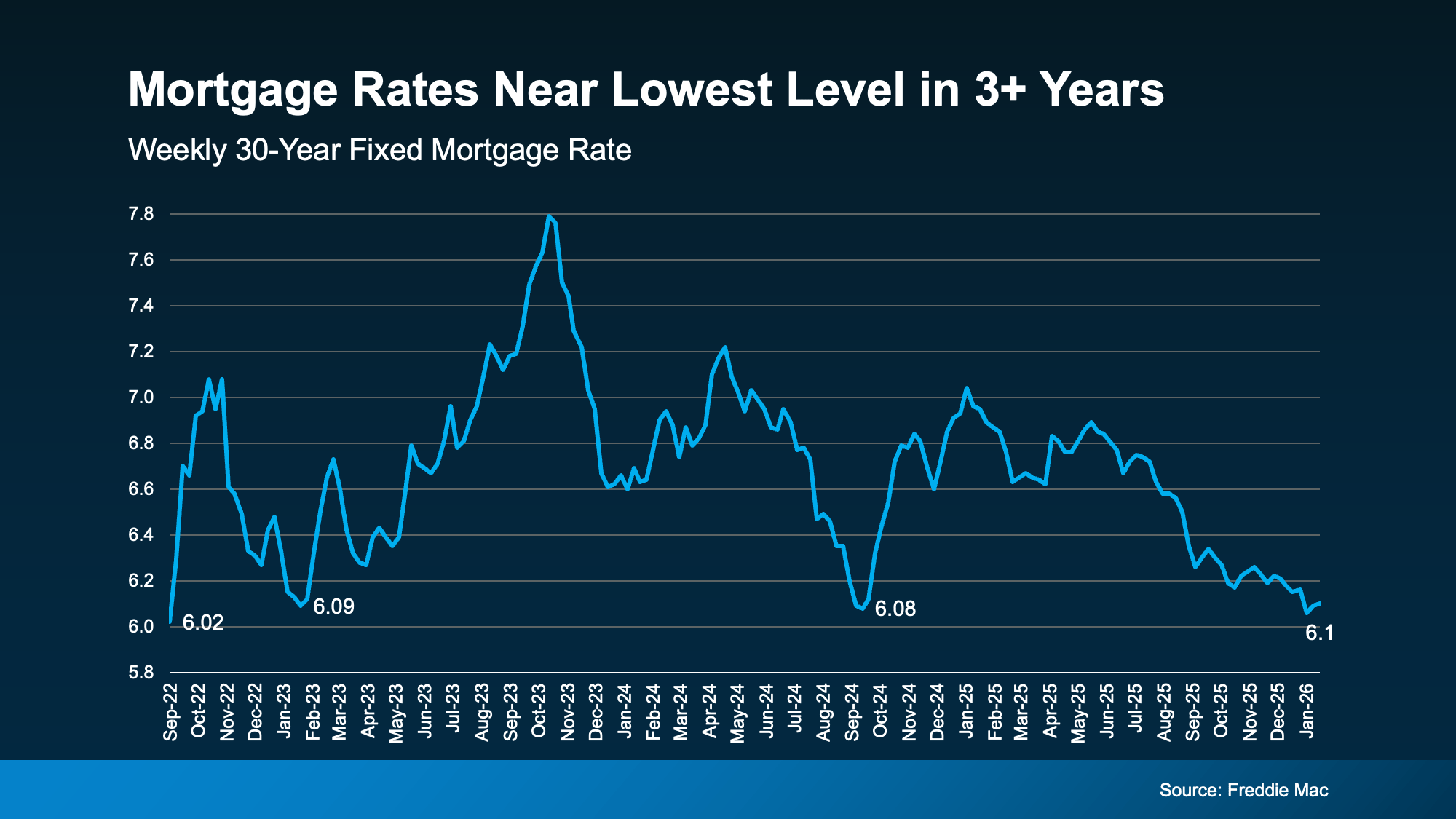

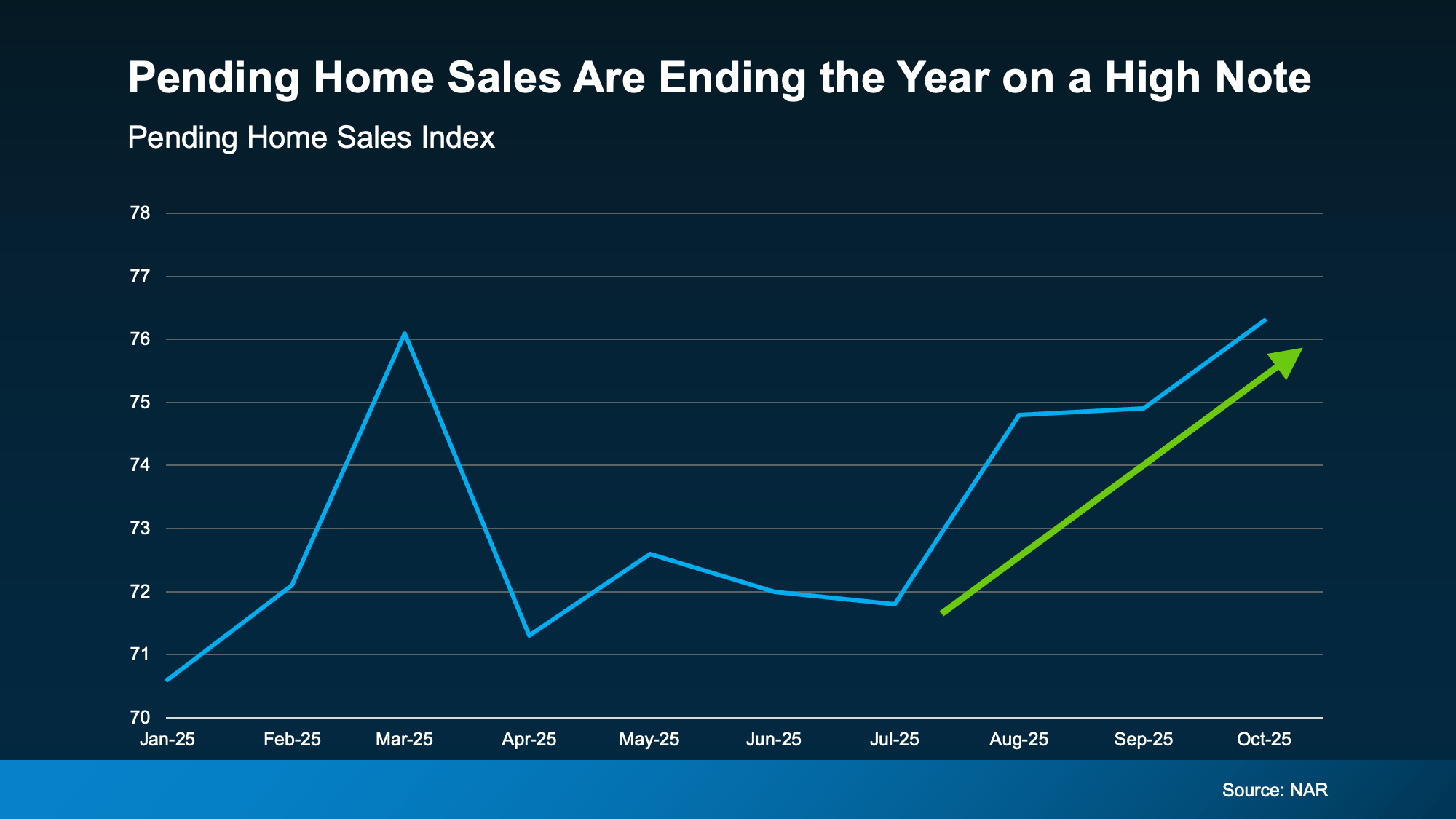

And that means the market is ending the year on a high note and headed into 2026 with renewed energy.

And that means the market is ending the year on a high note and headed into 2026 with renewed energy.