Whether you're dreaming about buying your first home or wondering if it’s time to move on from the one you're in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn't wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it's led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn't seriously considered before. As PODS, put it:

". . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

It’s Not Just the Home Price – It’s the Whole Cost of Living

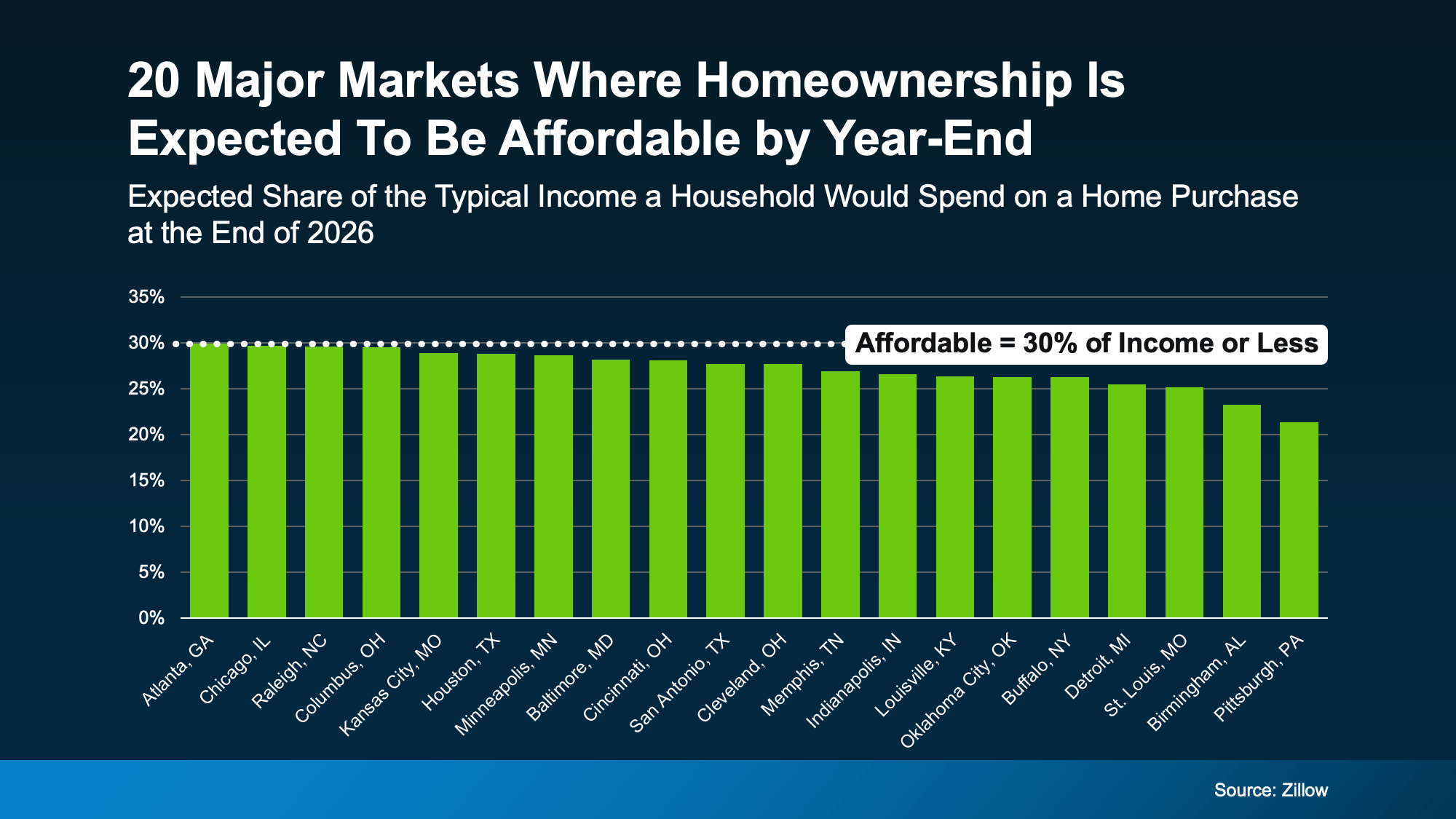

Here's where it gets really interesting. When people talk about moving for affordability, they're not just talking about finding a cheaper house. They're thinking about the full picture. What does it actually cost to live somewhere?

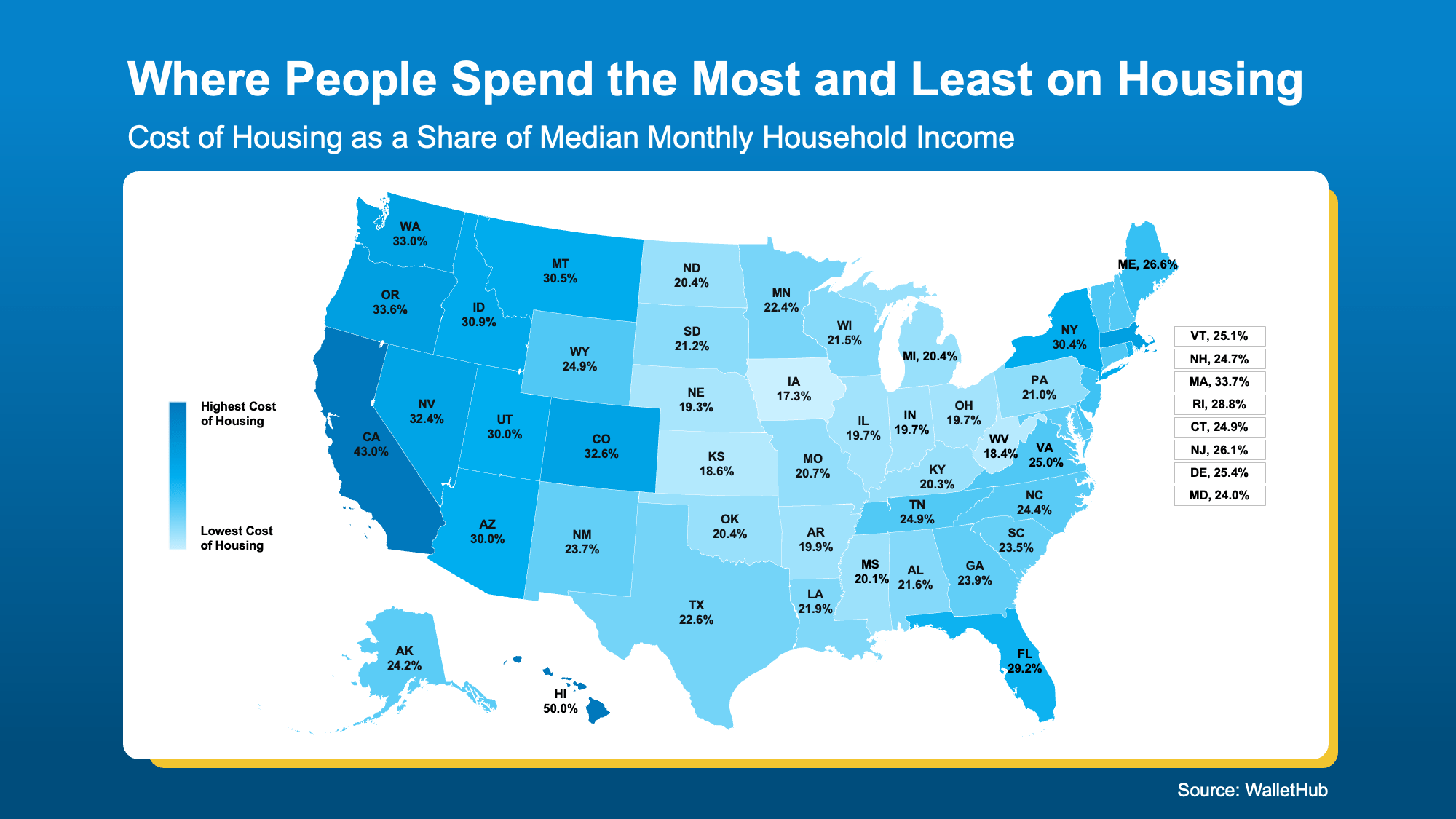

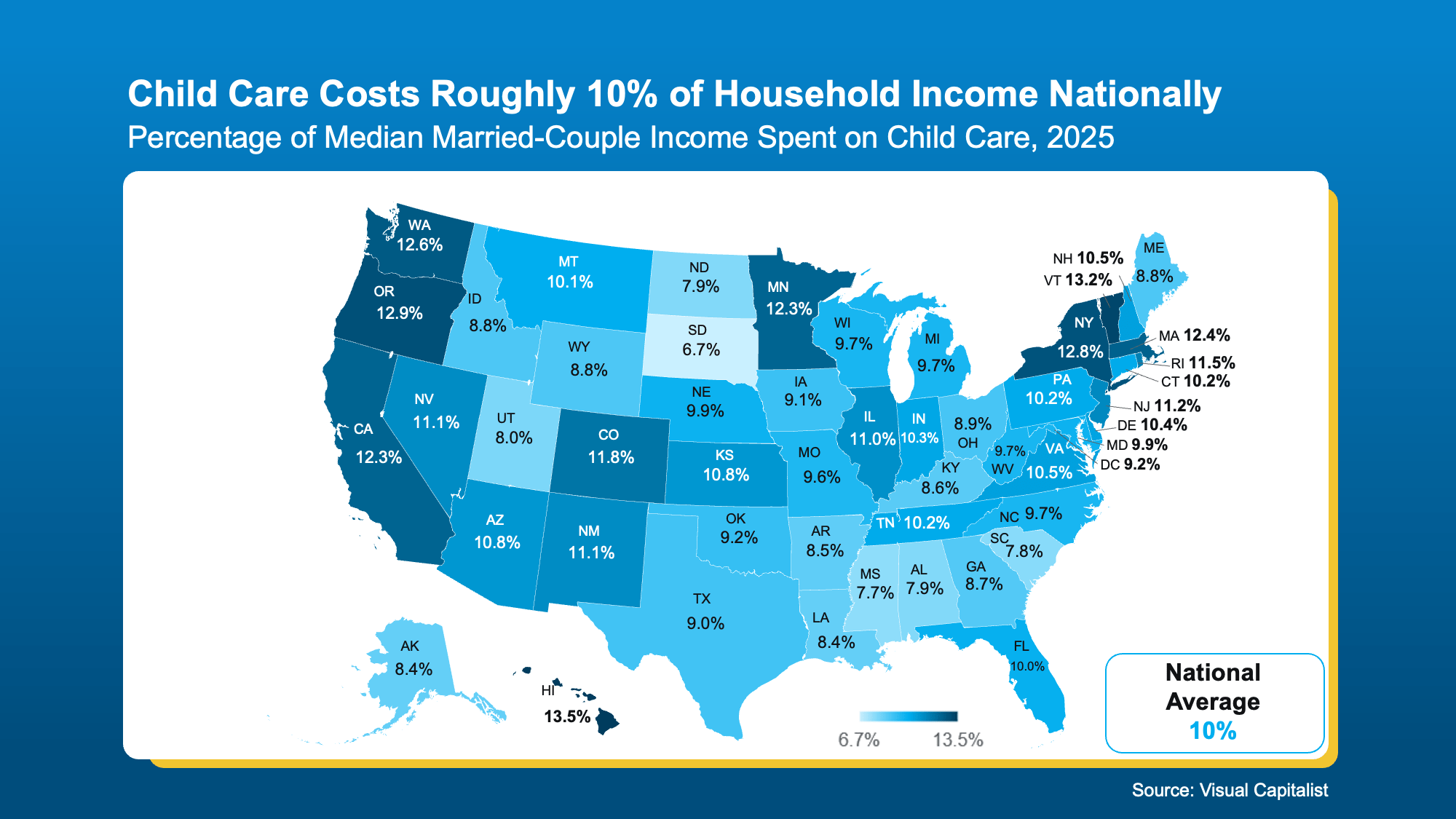

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you're less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

You Don't Have To Move to Another State To Find a Better Deal

But finding more affordable homeownership doesn't have to mean a cross-country move. It doesn't even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you're based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn't going away.

When location stops being tied to a daily commute, a more affordable area that's a bit farther out suddenly becomes a very real option.

Bottom Line

Affordability is a real challenge, but it's not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

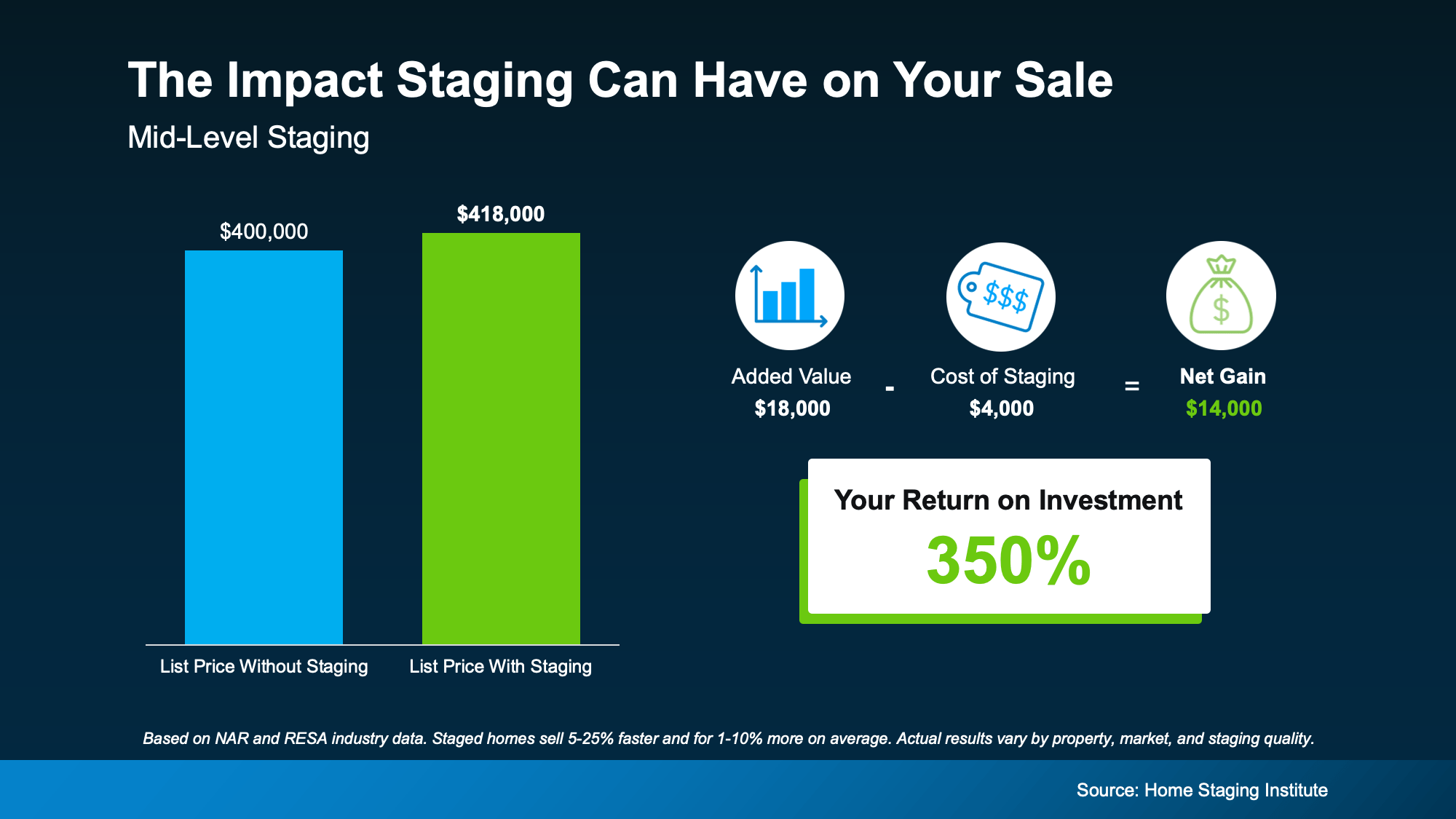

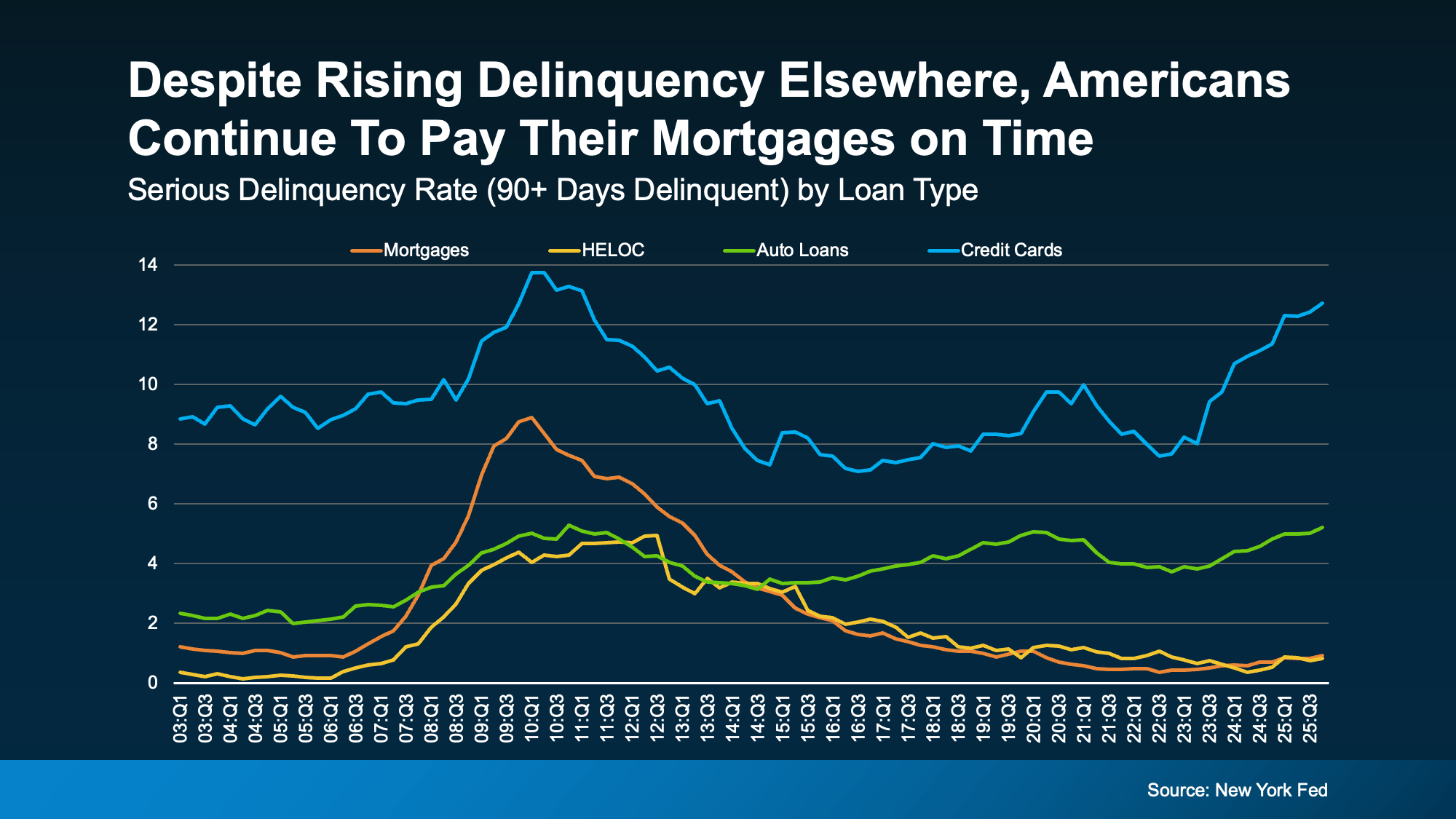

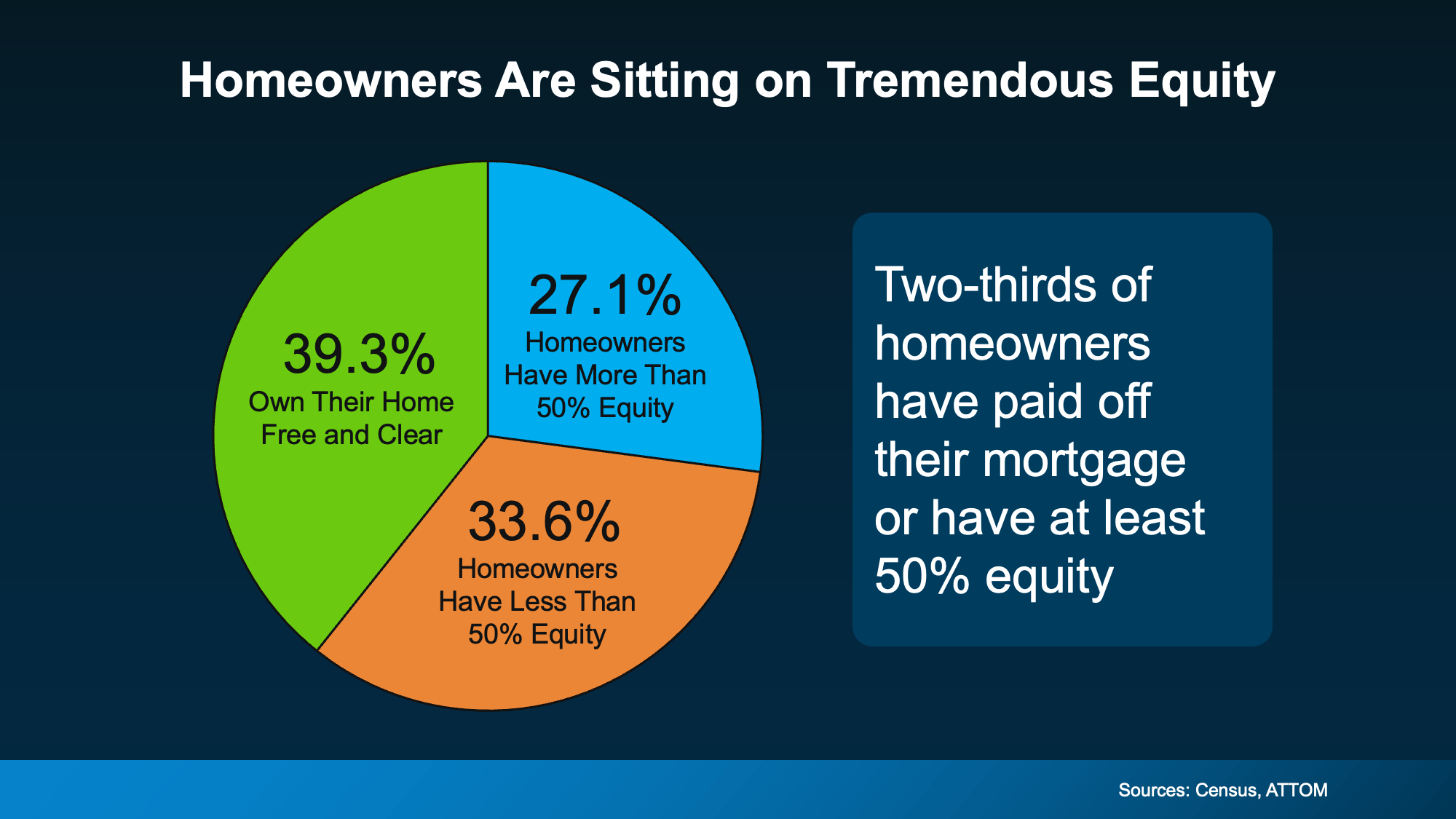

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

The Part Sellers Don’t See Coming

The Part Sellers Don’t See Coming