That kitchen you’ve been mentally redesigning...

The bathroom that really needs a refresh...

Or the outdoor space you keep saying you’ll get to someday...

What if you already have what you need to finally make it happen? Because a growing number of homeowners are realizing just that.

Homeowners are expected to spend over $522 billion on home improvements by the end of 2026 – and they’re not draining their savings accounts to get it done. Many are using their home equity.

And if you’ve owned your home for 10+ years, there’s a chance you could use your equity to fund some home upgrades too. Let’s break down what you need to know first.

What Is Equity? And How Does It Help?

Equity is the difference between what your house is worth and what you owe on your mortgage.

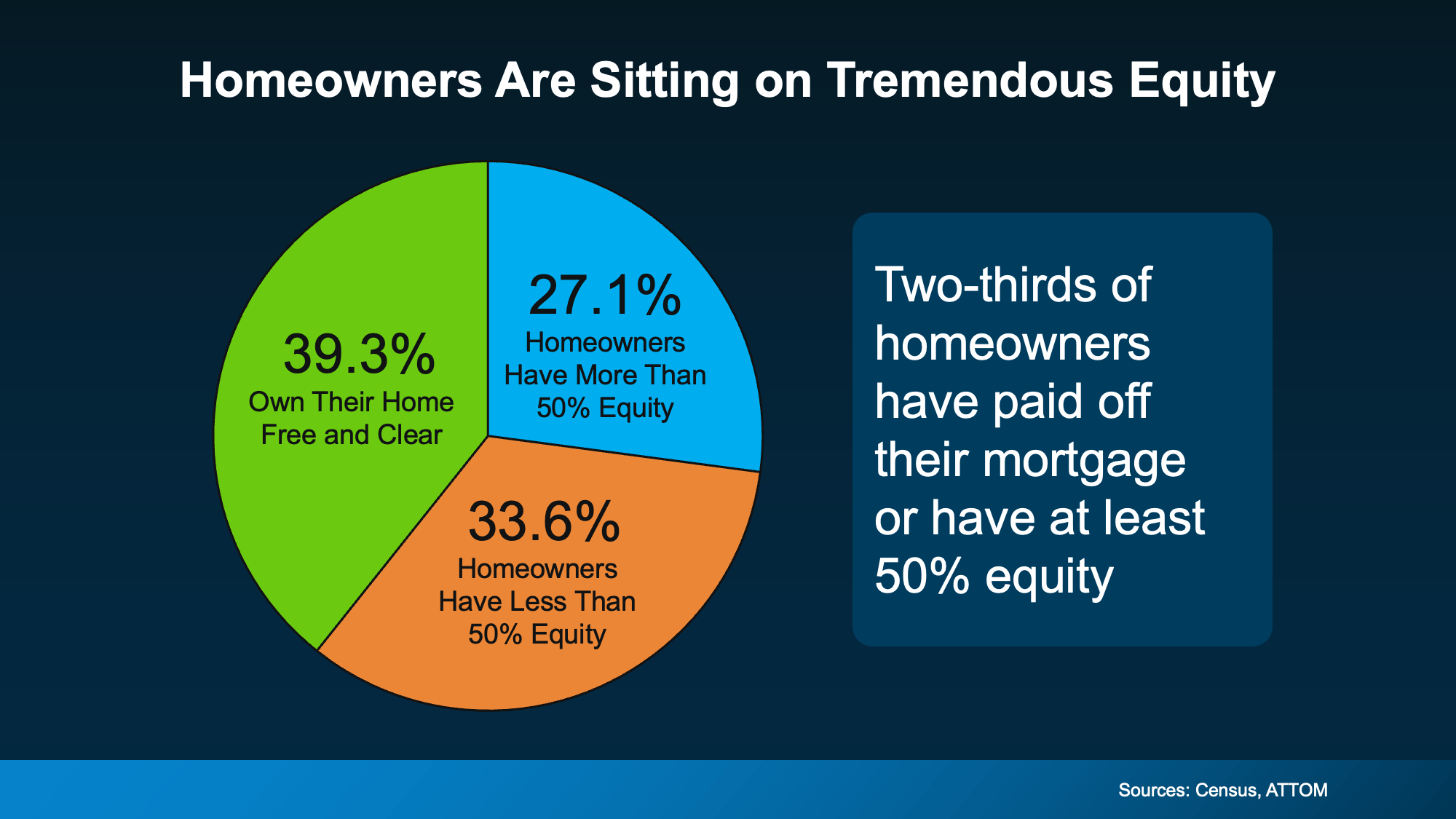

And according to Cotality, the average homeowner has about $313,000 worth of equity today. That’s more than enough to finally knock some projects off your list. And more people are realizing they can use that to give their home a little TLC.

Research coming out of Meridian Link says home improvements are the top thing people are using their equity for today.

Top Motivations for Equity-Based Borrowing:

- Funding home improvements (45%)

- Using it to pay down other debts / debt consolidation (16%)

- Investing in other properties (16%)

Maybe it makes sense for you to do the same. But here’s what’s important. Just because you can use your equity doesn’t mean you have to. It also doesn’t mean every project makes sense.

What Projects Are Actually Worth It?

If you’re going to go this route, you’ll want to focus on upgrades that actually pay off. A good renovation should be something that improves the value of your home. Because, even if you’re not planning to sell soon, you want to make sure you’re setting yourself up for success when you do.

And an agent is the best resource as you weigh your options. They know what other homeowners are doing and what buyers in your area like. And that can be really helpful as you narrow down your project list. As the National Association of Realtors (NAR) puts it:

“Being able to help sellers prioritize home improvements and maximize their net on the sale is a key value real estate agents offer.”

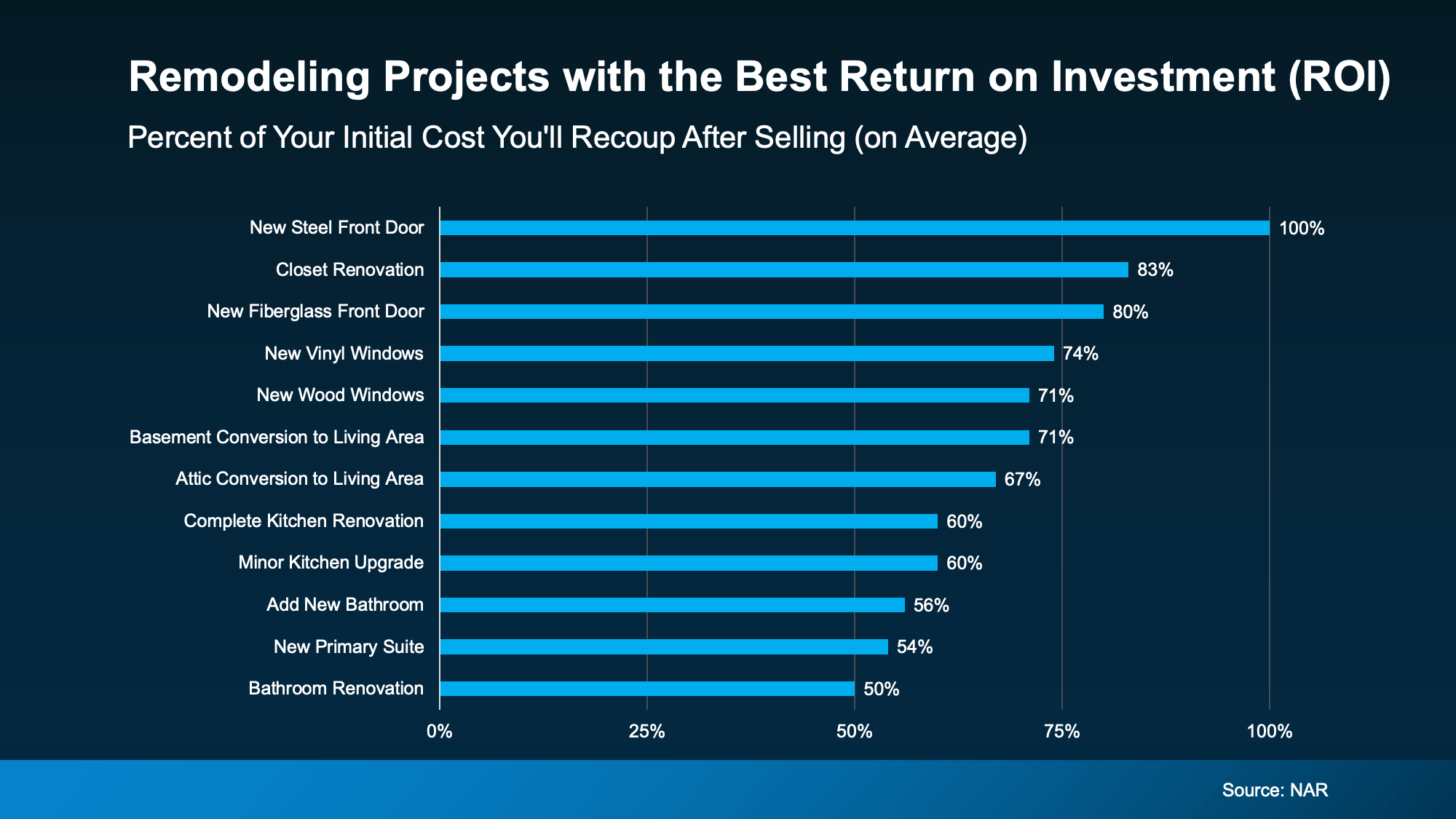

Here’s a quick rundown of the projects with the best potential to recoup your costs according to NAR (see graph below). While it’s a good starting point, just remember it can’t match the expertise an agent can provide.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

A new front door is a great project. But it’s not something to use your equity for. But revamping your kitchen? That’s where your equity can come in and lighten the load.

Where To Go from Here

Whether the project you’ve been thinking about is on this list or not, chat with an agent to make sure it’s worth the time, money, and effort before calling in any contractors.

Because the goal isn’t to do everything, it’s to invest where it counts.

And if you want to use your equity to get one of the bigger projects done, meet with a financial advisor too. Because you’ll want to make sure you’ll maintain a good loan-to-value (LTV) threshold even after using your equity. That way you have all the information you need to make your decision.

Bottom Line

Whether you’re selling next year or just giving your house some TLC, the right home improvements today can set you up for success tomorrow. And the best part? Your equity may be the key to making it happen.

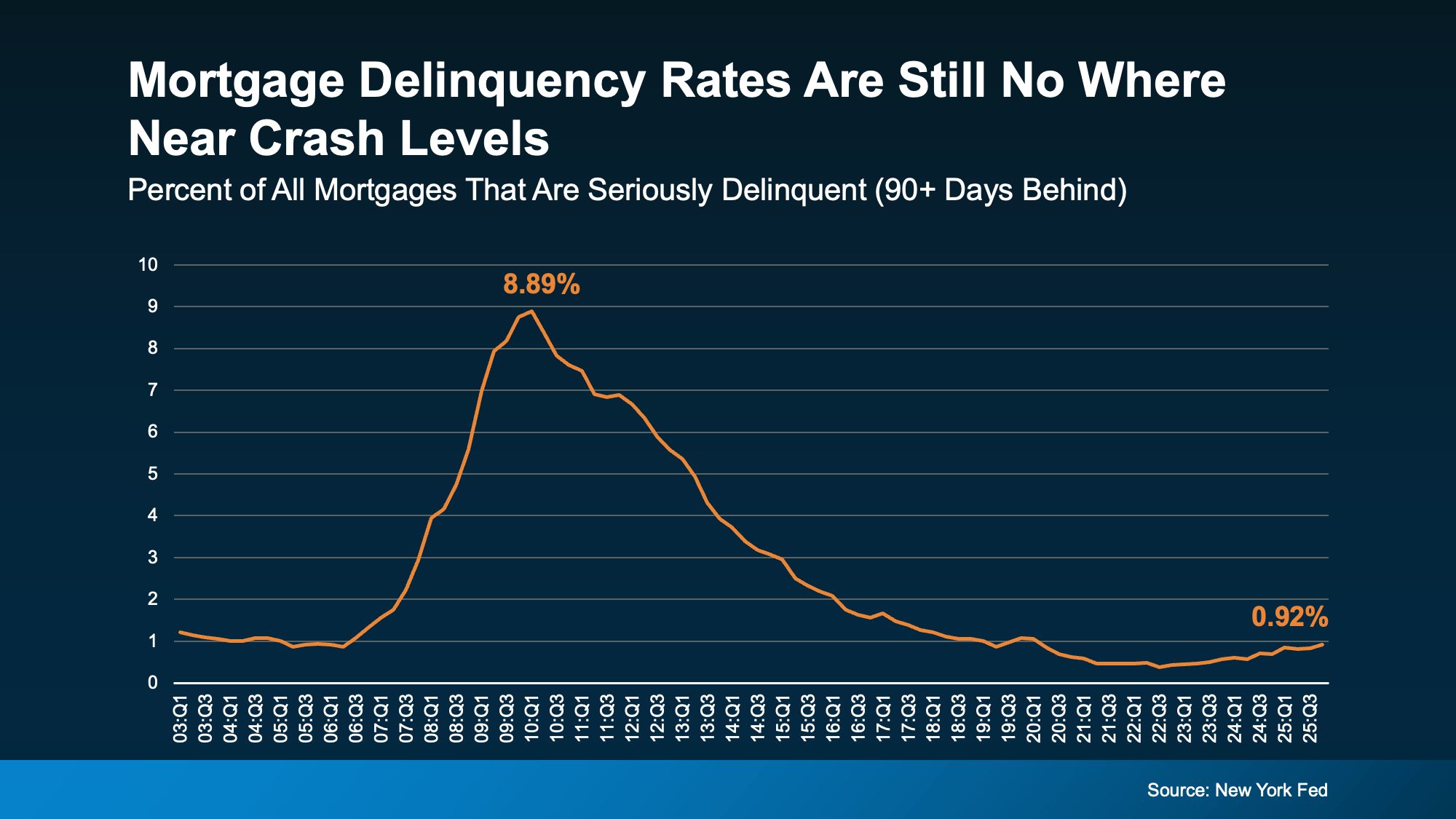

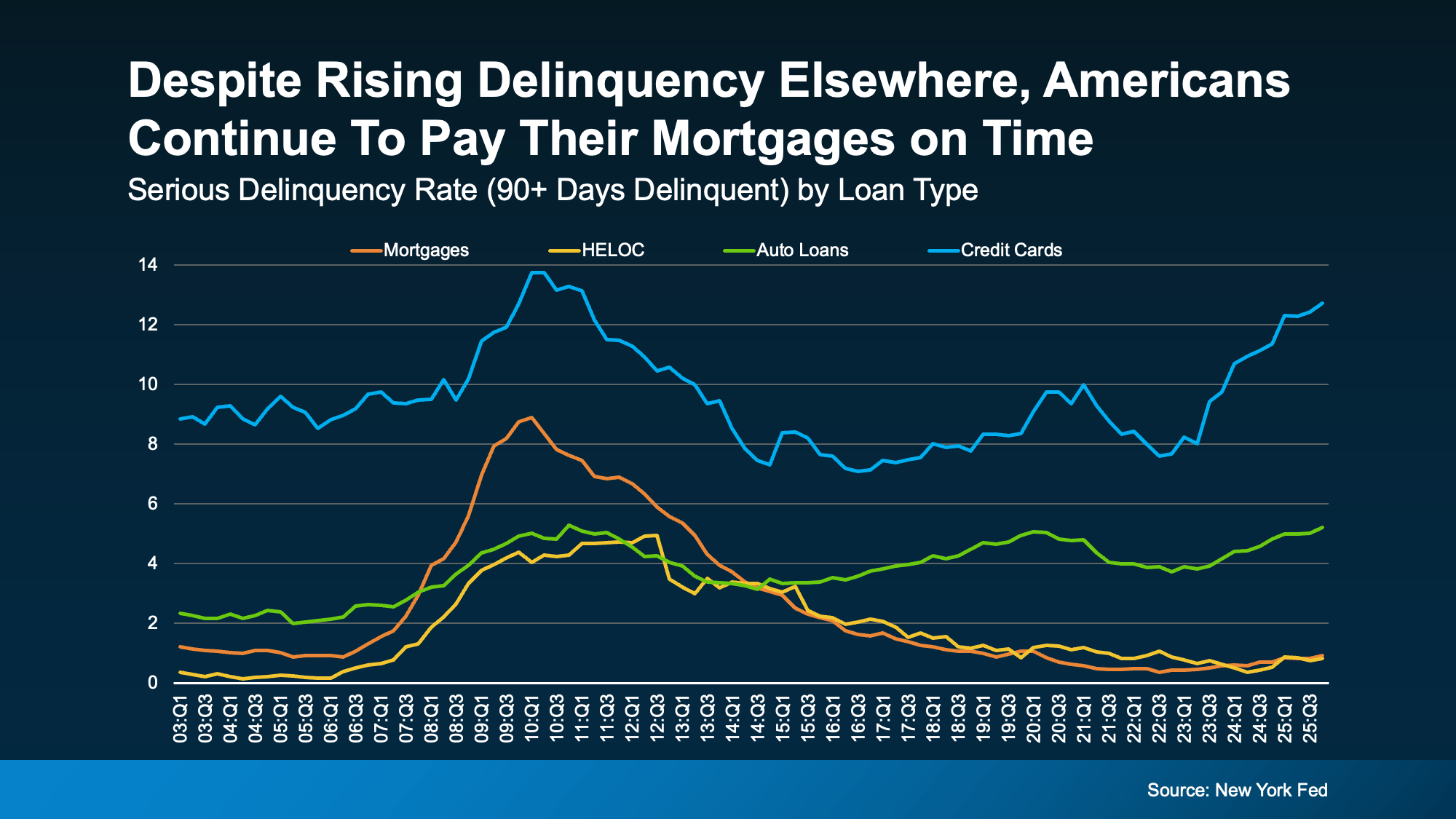

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

The Part Sellers Don’t See Coming

The Part Sellers Don’t See Coming

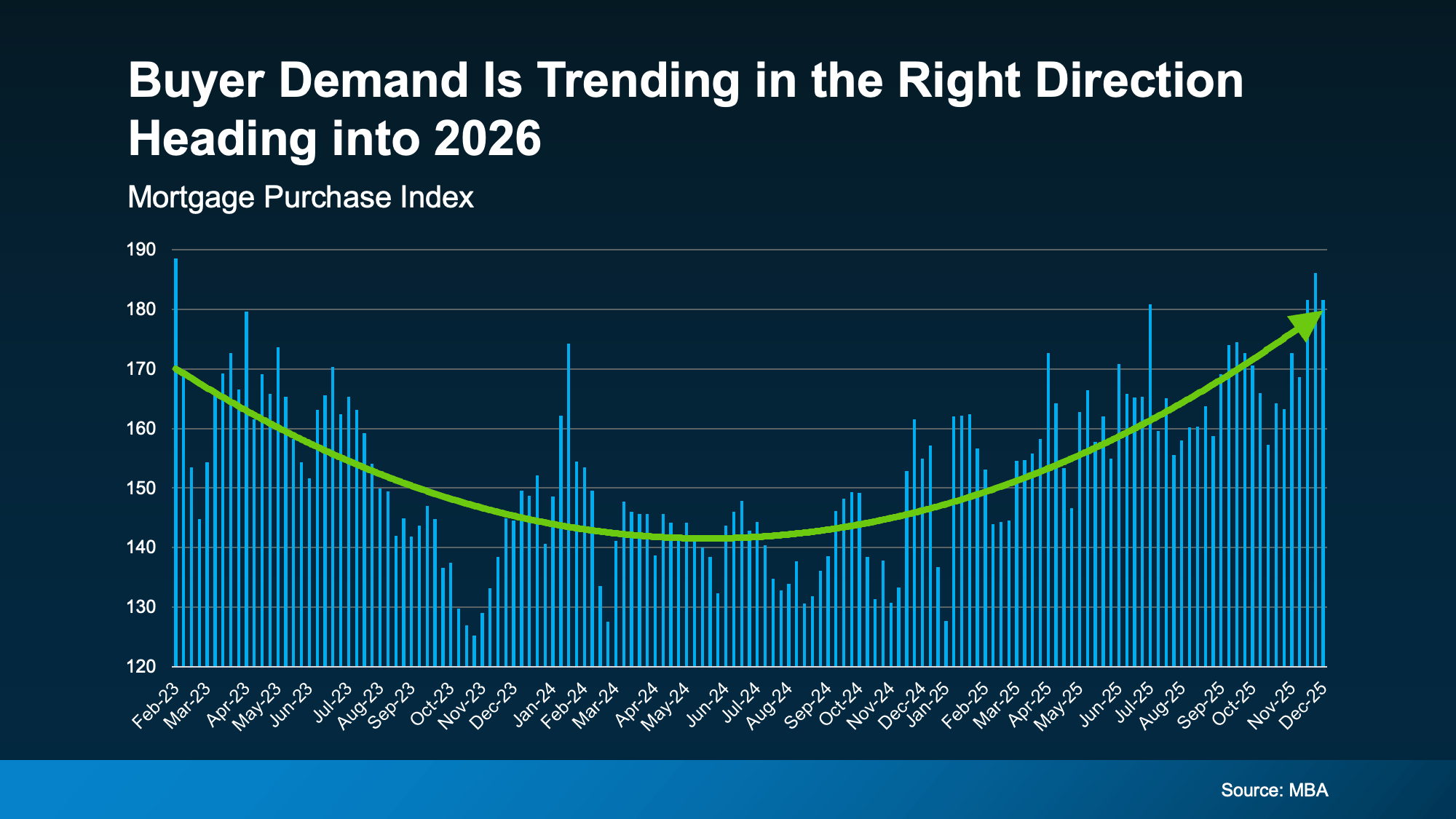

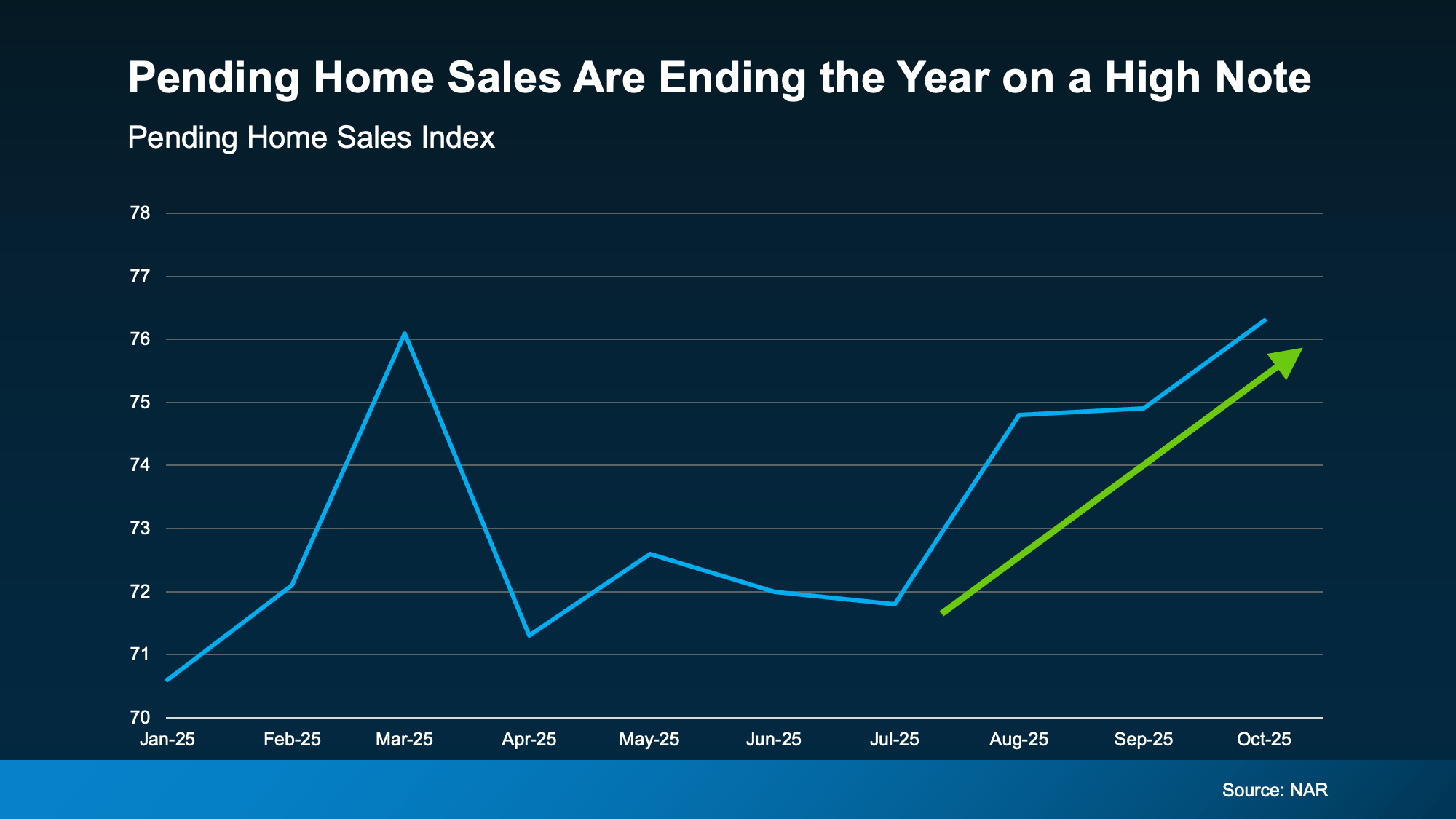

And that means the market is ending the year on a high note and headed into 2026 with renewed energy.

And that means the market is ending the year on a high note and headed into 2026 with renewed energy.