You’ve probably asked yourself lately: Is it even worth trying to buy a home right now? It’s a question a lot of people are asking.

With today’s home prices and mortgage rates, renting can feel like the easier path. In some cases, it might even seem like the only realistic option right now. And if that’s where you are, there’s nothing wrong with that.

But if you’re weighing the decision, there’s one part of the conversation that doesn’t get talked about enough.

It’s what each choice does for your future.

What Renting Really Gets You (And What It Doesn’t)

Depending on your situation, renting does have some advantages:

- Lower upfront costs.

- Less responsibility.

- More flexibility to move when you want.

But even with those benefits, a Bank of America survey found 70% of aspiring homeowners worry about what long-term renting means for their future. And that concern comes down to one thing: you’re not building anything for your future. As Yahoo Finance explains:

“Paying rent doesn't build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So, while renting may feel easier, the flexibility you get comes at a cost.

How Homeownership Builds Your Wealth Over Time

On the other hand, owning a home is one of the most consistent ways people build wealth over time. Why? When you’re a homeowner, you gain something called equity. That’s the difference between what your home is worth and what you owe.

That equity grows with every monthly payment you make. It also gets a boost as home values go up through the years – and it adds up quicker than you may think.

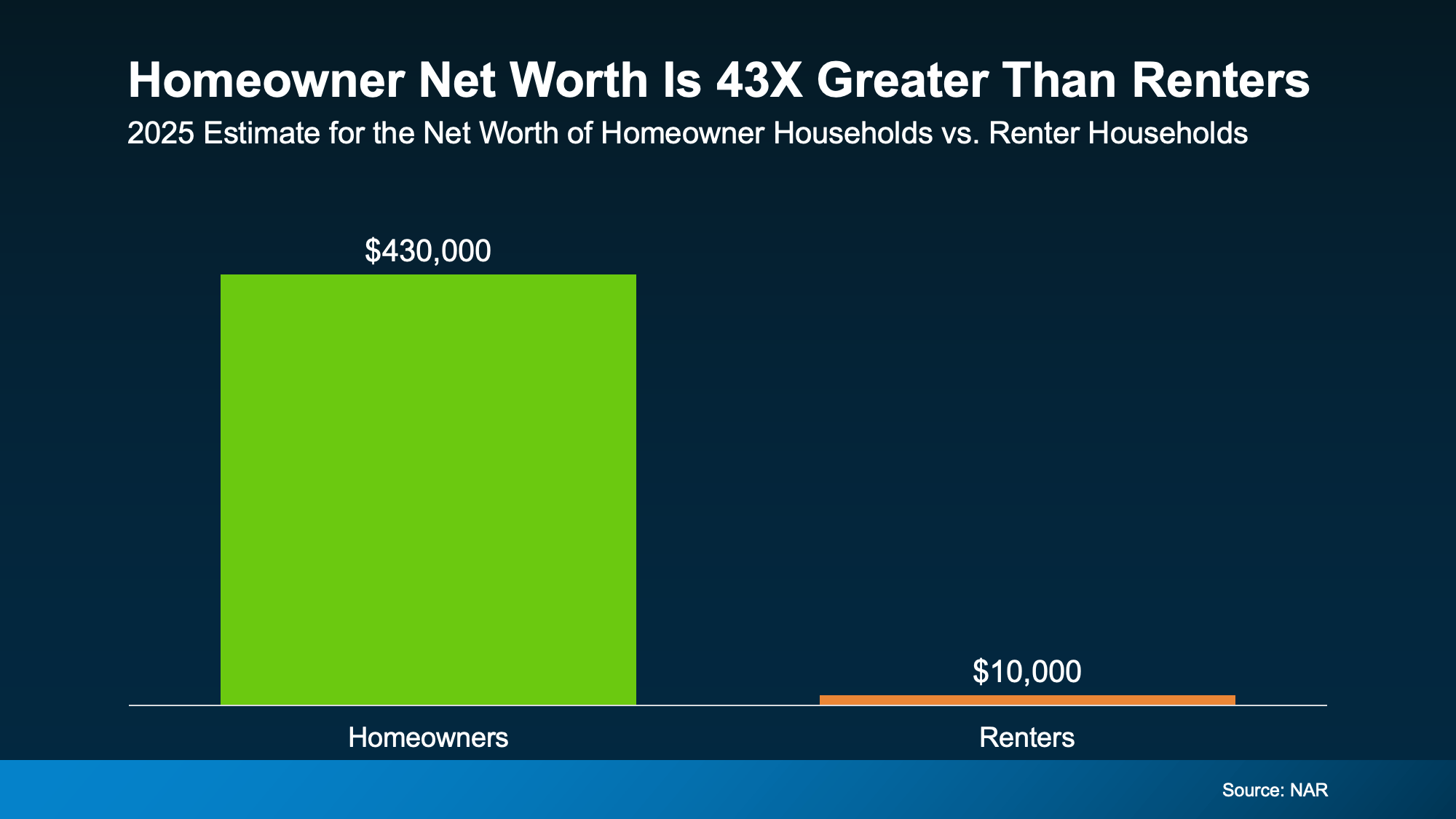

Today, the National Association of Realtors (NAR) says the average homeowner’s net worth is 43X greater than that of a renter:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

- Homeowners: $430k

- Renters: $10k

And it’s not because homeowners make wildly different decisions day to day. It’s because over time, one path builds something, and the other doesn’t.

So sure, buying comes with some upfront costs and more responsibility. But it’s basically a savings account you can live in.

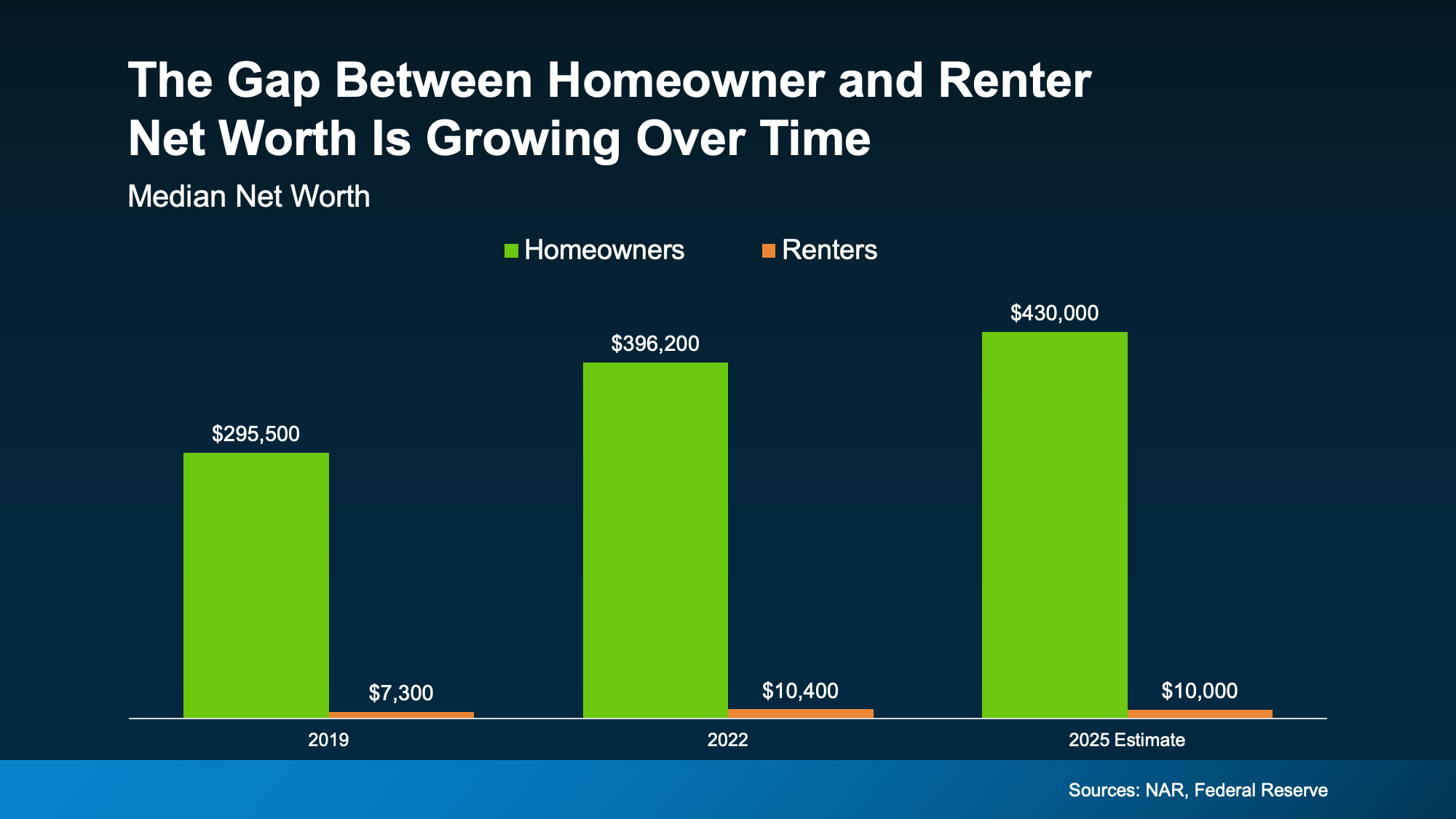

The Gap Is Growing Over Time

And here’s something else interesting. That net worth gap between renters and homeowners has been widening over time, not shrinking.

If you look back at the reports on net worth through the years, you can see the gap is growing as homeowners gain wealth and renters stay stuck in the rental trap (see graph below):

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

When you can afford it and you’re ready for the responsibility, history shows buying is usually worth it in the long run. Because either way, you’re paying for someone’s mortgage and building someone’s net worth.

When you rent, it’s your landlord’s mortgage – not yours. But when you buy? Your monthly payments help build equity.

The question is: whose do you want to pay? Yours or theirs?

So, Should You Buy a Home Now?

The short answer is, it depends on your situation.

While the long-term benefits of buying are clear, that doesn’t mean the timing is right for everyone right now. And that’s okay. You should only buy a home once you’re ready and the numbers work for you.

But whether you’re looking to buy now or planning for the future, the first step is the same. You should have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you run the numbers and see what’s realistic. You may find buying is closer than you thought. And if not, you’ll at least know exactly what it will take to get there.

Because the sooner you have a plan, the sooner you can decide when it makes sense, instead of wondering if it ever will.

Bottom Line

Renting may feel more do-able today. But over time, it could cost you.

If you want to ditch renting and start building something for your future, it starts with a simple conversation. Let’s connect, talk about your specific goals, and explore your options – so you’re ready when the time is right for you.

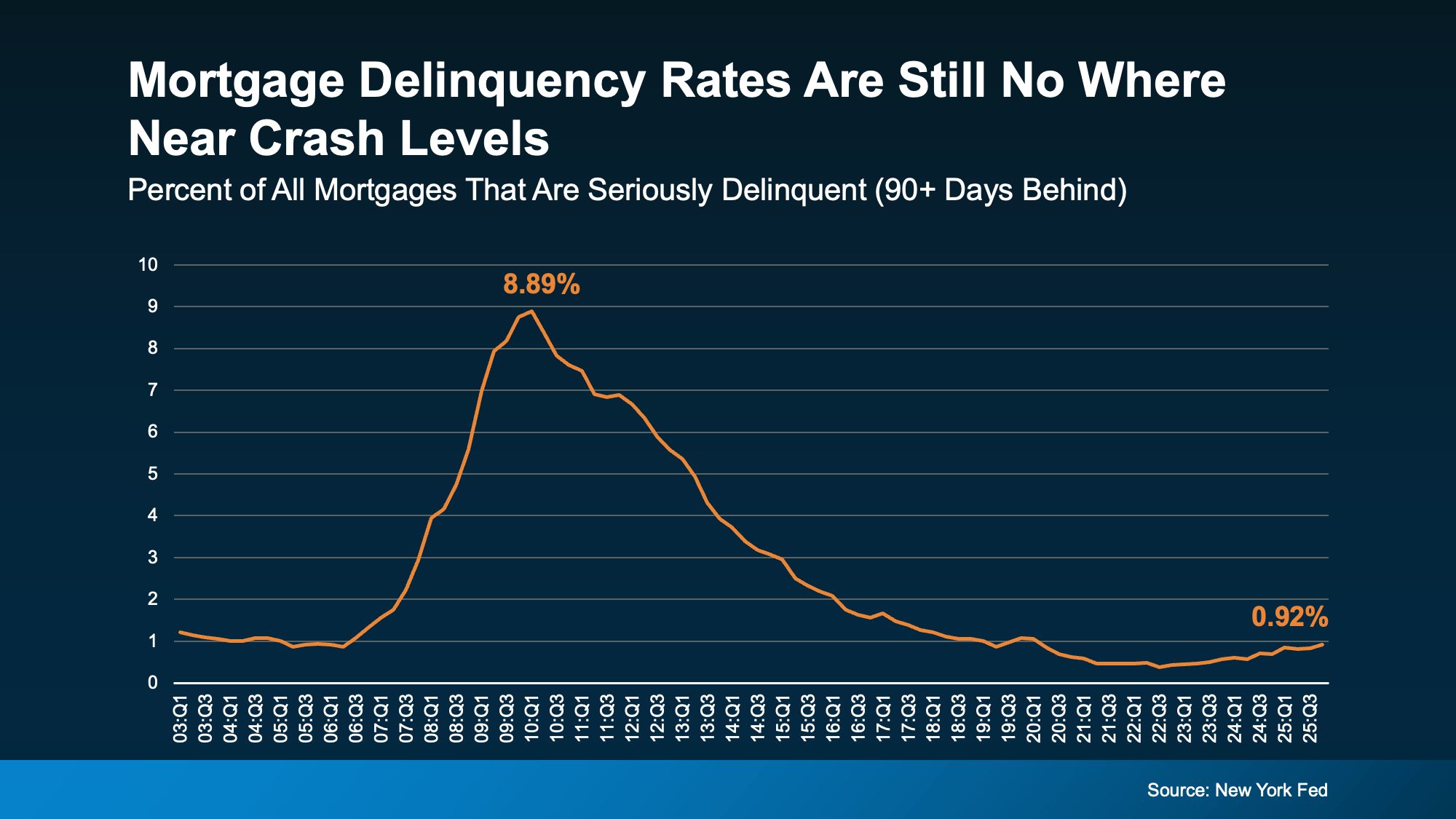

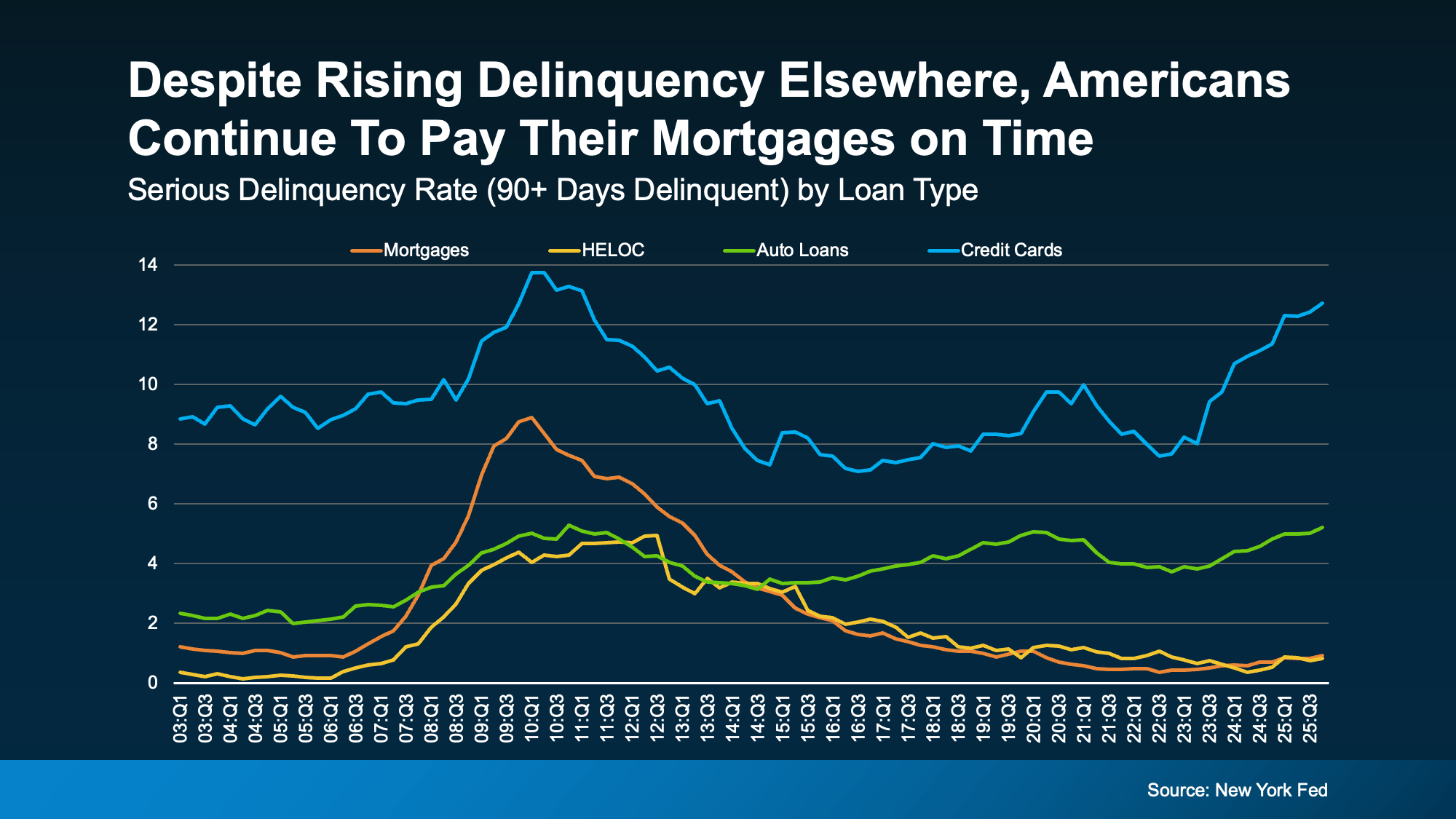

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

The Part Sellers Don’t See Coming

The Part Sellers Don’t See Coming

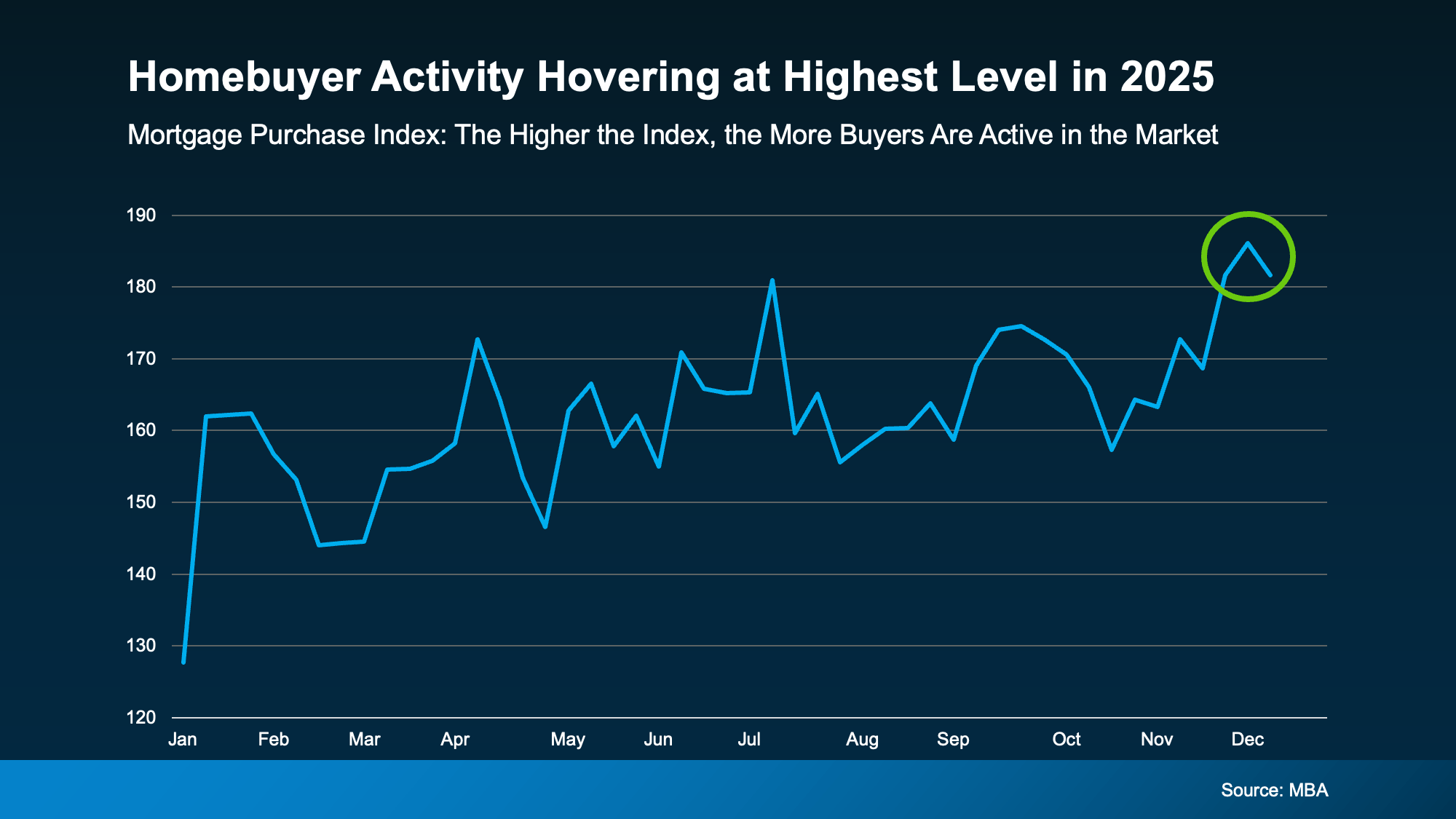

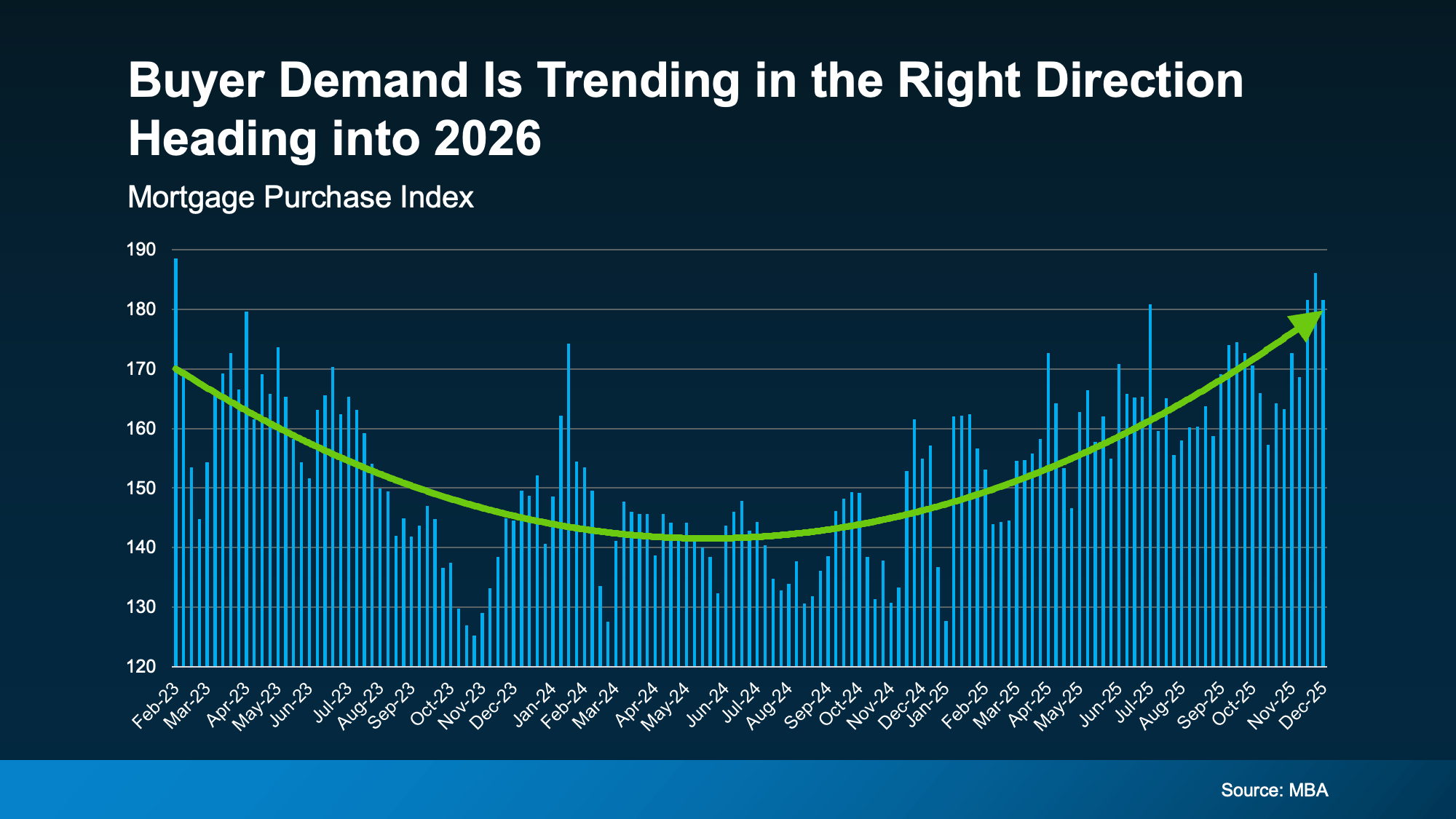

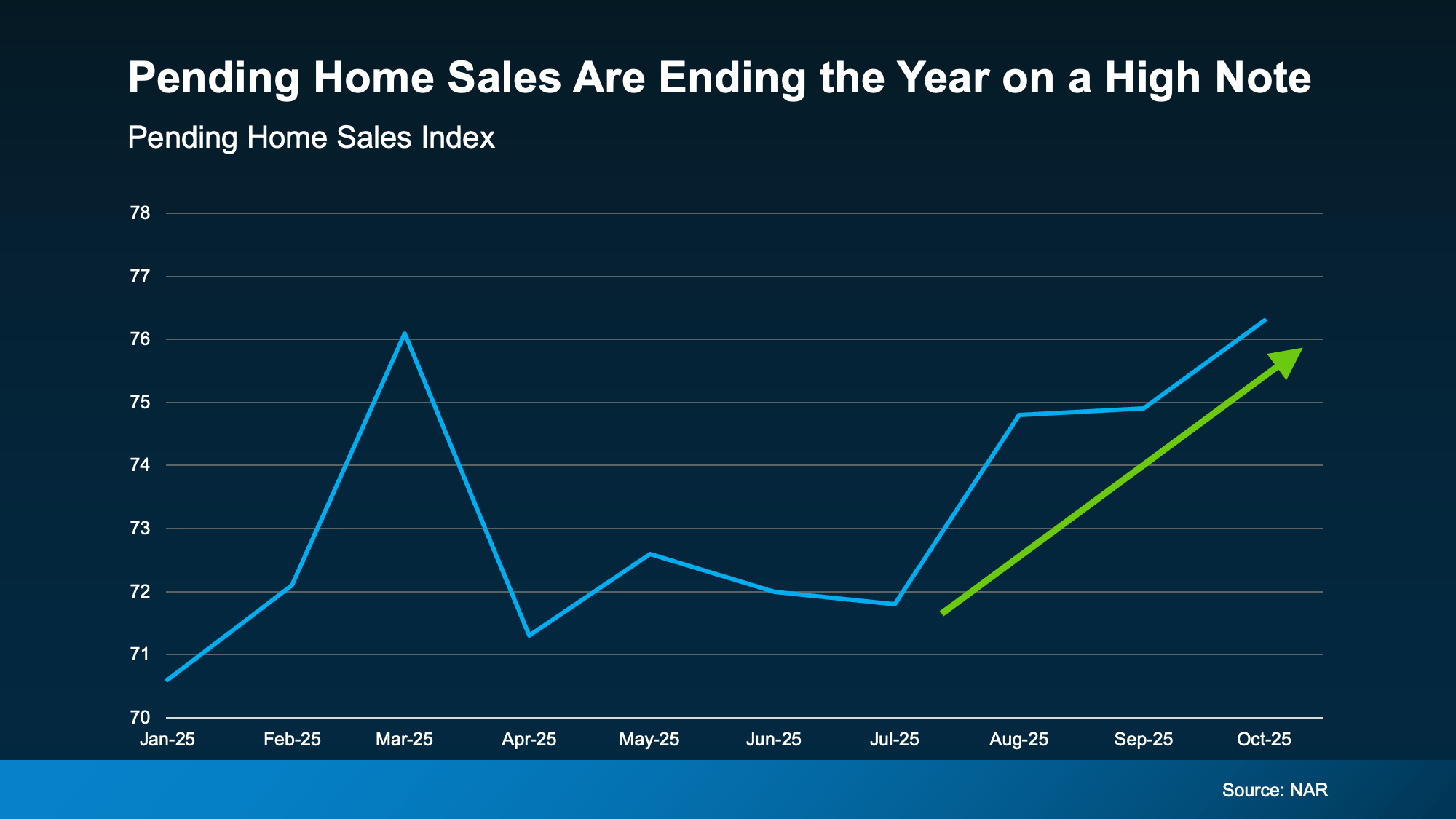

And that means the market is ending the year on a high note and headed into 2026 with renewed energy.

And that means the market is ending the year on a high note and headed into 2026 with renewed energy.